As long as you are not in the first year, you can of course do whatever is easiest.

I believe they would refund the difference in fee if you downgrade within 30 days after the annual fee hits - and you might want to wait until your 9K annual points hit your account if you can before the 30 days are up.

I was thinking this if I don’t risk the credit in fees. For the extra $150 I don’t see the value- for us anyway. Do they happen at the same time- the fee and the annual points credit?

Whoops: I typed up the wrong suggestion below - it was not $5 back for buying something in Holiday wish list - it was spend $100/back from Holiday wish list get $15 back. Much better!

I fixed the #braincramp info below.

Also note: look to see if you have a Target circle offer in your account that gives you $15 back for spending $100 in your Holiday wish list. I do not have that offer, but someone else reported adding the gift card to their wish list before purchase and it stacked on the other offer.

Also, FWIW, a few weeks ago I had a circle offer for $10 if I just added 10 things to my holiday wish list. 10 seconds of clicking later and I had the $10 in my account. Worth looking to see if you have that one too.

Does Citi have a similar limit like Chase does 5/24? I’ve just noticed a lot of our store cards are Citi. Not that I plan on opening a bunch of Citi cards but just wanted to be aware if their was a limit.

Currently working on next year’s budget and bill pay worksheets. I like to set the WHOLE year up in advance. This really makes paying bills and tracking budgets a breeze throughout the year.

I just started thinking about this today. We did open an AA card for a great miles SUB. May do the Strata Sub down the line if we see a decent offer. So no plans to open a Citi card soon for now. Will have to research it a bit.

This is not a great return on spend for $6K - I would prefer to be getting at least 50K MR or more.

But sometimes when you are in between Sign Up Bonuses (SUBs) getting a quick fill business card helps juice up your points earning on spend a little without affecting your 5/24 count. and I’ve done so.

Plus, I’m sure I’ve said all this above in thread, but worth saying again:

As a no annual fee card it is nice to have to hold your Amex MR if you decide to close your other Amex cards AND usually 0% interest for the first year so you can play the float: Keep your cash in your high yield savings account for most of that year to earn some extra interest, then pay it off in one swell foop. (You have to make minimum monthly payments all that time of course.)

I didn’t have that one, but had $20 back for $200 in qualified spend, which includes gift cards (as long as they aren’t branded as credit cards.)

I bought 2 $100 gift cards in separate transactions and received the $10 target GC for each transaction, plus the 5% for circle (and crossed the threshold for the circle bonus ($20)

On the app. Would purchase $100. It showed 2 items in cart ($100 disney gift card and $10 promotional target gift card). Purchased. Received both so purchased another. After 10 it canceled. Ended up doing it under spouse account after that to get more.

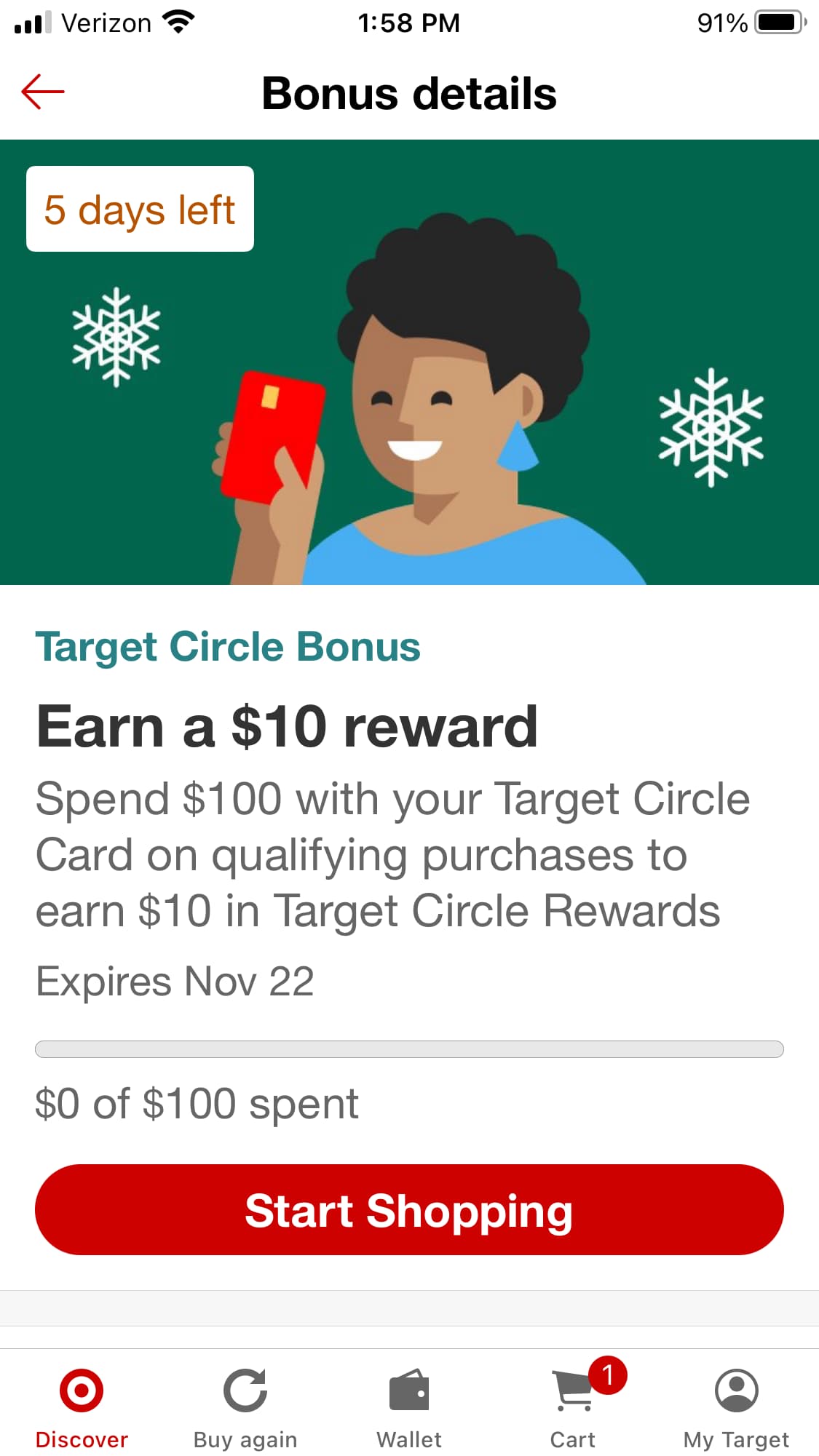

Ok, so I just bought a $100 Disney eGift card from Target. I got a $10 Target gift card and 5% off ($90 x 5% = $4.50) by using my Target card. I also earned $10 in Target Circle rewards with this offer:

Another opportunity for gift card purchases for folks with an Amex Platinum card:

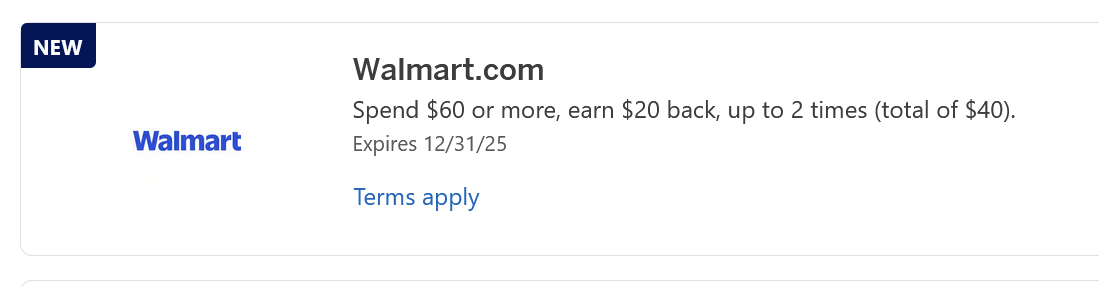

Check your offers for a spend $60 get $20 up to 2 times offer. (Remember you have to add offers to your card before using!)

Read the terms just in case, but from what I saw in a points group and my past use of this same deal: while the terms exclude BULK gift cards and E-gift cards, you can order physical GCs and the credit should work.

Also, this offer is for online at Walmart.com and not in store - of course, you can place an online order and set it up for pickup if you really wanted to.