Okay, that sounds slightly less sketchy!

3 Likes

Doctor of credit has a link for Delta business cards that have no lifetime language. Meaning you can get a card even if you already had it previously. I have had the Delta gold business card for less than a year and was just approved for another.

4 Likes

Hadn’t done it before but new Ink cash card only had 4k in spending limit so called in and moved spending limit from my ink preferred card. Only took 2 minutes. Definitely going to do that in the future with new Ink cards.

2 Likes

I used your spreadsheet link @JJT and was approved for the Amex gold—it’s nice to have a SUB to work toward after an unexpected storm last weekend convinced us it’s time to have two big trees removed from the yard. Enjoy the federal bonus points!

I haven’t had an Amex before, looks like some interesting new benefits.

4 Likes

Thank you!

The Gold is probably the best all around Amex card IMHO.

4x points on grocery and restaurants - the grocery for us really racks up points with our family spending.

The monthly $10 dining, $10 Uber and $7 Dunkin credits cover much of the annual fee.

The new $50 Resy credit every 6 months was a complete bonus for us, really puts it over the top.

4 Likes

Want to add a modifier to this statement I made back in May with my silly meme: In reality Marriott points CAN expire, I think with 2 years of no activity.

BUT: it is really easy to keep them alive: earn new points over time (spend on credit card), transfer some points in, even if just 1,000 points etc.

1 Like

| Sometimes points are a little scary. Spending $1,012.99 at the grocery store for some plastic cards and a pack of gum can be (ooh I just realized I got my gum on sale.) |

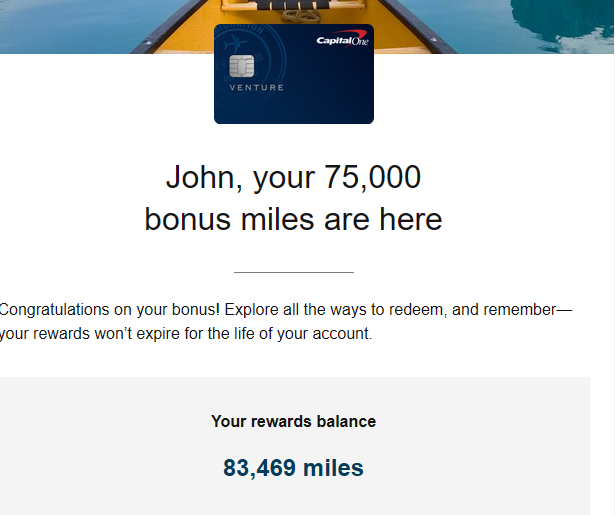

I recently hit my spend on the Cap One Venture card and earned my bonus and right now I’m in between sign up bonuses. We have been kind of busy and I like to have the next few steps of my plan ready to go, and I ain’t done that yet.

So, right now I’m falling back to using various cards in hand for the best points earning I can muster under the circumstances.

I have some college 529 deposits to make for DD, some college loan payments we need to do for DS, as well as the usual miscellaneous spend on utilities and churro supplies.

Visa & MasterCard Gift Cards at Office Supply

For the latter, I ran over to my local Staples to pick up some $200 MasterCard gift cards during the current fee-free promotion on those. Using my Chase Ink Cash there at 5x points, that is a sweet 1,000 Chase Ultimate Rewards per card.

Sadly, someone else had wiped out most of the inventory, so I only scored one card so far - but used that for my electric payment as soon as I was back at my computer.

Gift of College

Another method of spending that I have dabbled in over the years is purchasing Gift of College cards - long story short on those is they are a gift card-y thing that you can buy and send to 529 plans and sometimes to pay college loans. (Paying college loans is YMMV depending on the loan servicer. You may have to be your own data point here for some of them.)

GoC cards do charge fees, so you want to make sure that the fee you pay is worth the squeeze of the points. or some such metaphor. Often the no-brainer time to buy them is when you are working on a sign up bonus for a card since you will be earning a large multiple of points per dollar spend.

NOTE: Do NOT buy GCs when working on an Amex bonus - they don’t like GC spend for SUBs.

Sadly, GoC cards (or at least the better value ones) are not available widely everywhere - even though they are supposed to be sold at Cumberland Farms, none of the local ones here carry them. While CVS does carry them here, theirs allow a lower maximum amount of $200 and thus the fees end up being a higher % per dollar, so that is much less than optimal and I had mostly forsaken using them unless I really needed to hit some extra spend to reach a bonus.

There was an exciting news a month or three back: Stop & Shop and Hannafords started carrying GoC cards - and they were the ones loadable for $25 to $500 each, making them the best deal when you max out the card.

The fee to load the card is $5.95 no matter how you slice it - so as you can see below, loading just $25 is a suckers game, while adding the whole $500 is the hero’s game.

Worth It?

In today’s instance, I used my Cap One Venture to earn 2x points on GoC spend. So $1k cards with about ~$12 in fees earned about $29 in conservative points value if I transfer those points to travel partners. Not a terrific turnover by any means - but I am even ahead by several ![]() even if I just cash the points out for 1 cent each as I discussed previously in the thread.

even if I just cash the points out for 1 cent each as I discussed previously in the thread.

Is that worth it? Probably? Maybe?

In reality I will likely focus on buying these in the future when I am back on earning a SUB and getting many more points for the spend. Or, I will use some other cards that earn points where I have a better chance using them for 2 cents per point (cpp) than the Cap One miles.

For example, my Chase Ink Unlimited earns 1.5x everywhere - so instead of 2,000 Cap One Miles, I’d only have 1,500 Chase UR - but I often get 2 cpp or more at Hyatt with those. My Amex Blue Business Plus also earns 2x everywhere, so another good alternative.

If you would like to read more about Gift of College tactics, Frequent Miler has had a post about them for years where you can study up.

Also see this more recent short update of a post when GoC began appearing at Stop & Shop & Hannafords.

1 Like

small win with my Citi Freedom card over the weekend. I’ve been dabbling with the idea of a quick pop into the World for my birthday weekend (11/01 - 11/03). But I’ve kinda already allocated my 2025 travel money. I have a variety of points but do I want to use them?..

Well, through the Citi travel portal, Swan with a refundable rate was only $250 a night. This is about $130 less per night than booking through Marriott direct when I checked. Pop Century was even more than $250. And I didn’t use my points so when the charge hits my card Ill get 4 X’s the points back plus a little $30 (or $50, cant recall) statement credit through a promotion for booking through the Citi travel portal through August. Will use points for statement credit though.

Plus my preferred flights on SW are only 5,000 each way! (For 2 since DH is my CP through the end of this year).

So now all I have to work on is how to pay for tix. Still not 100% decided. But I’ve booked the hotel and flights preemptively. Interestingly, the Swan Reserve and the Dolphin had a memo of X amount for the night plus the resort fee. Swan didn’t mention the resort fee. Probably just a typo. Guess I’ll be charged at the resort. But it would be a happy little glitch if I didn’t…

3 Likes

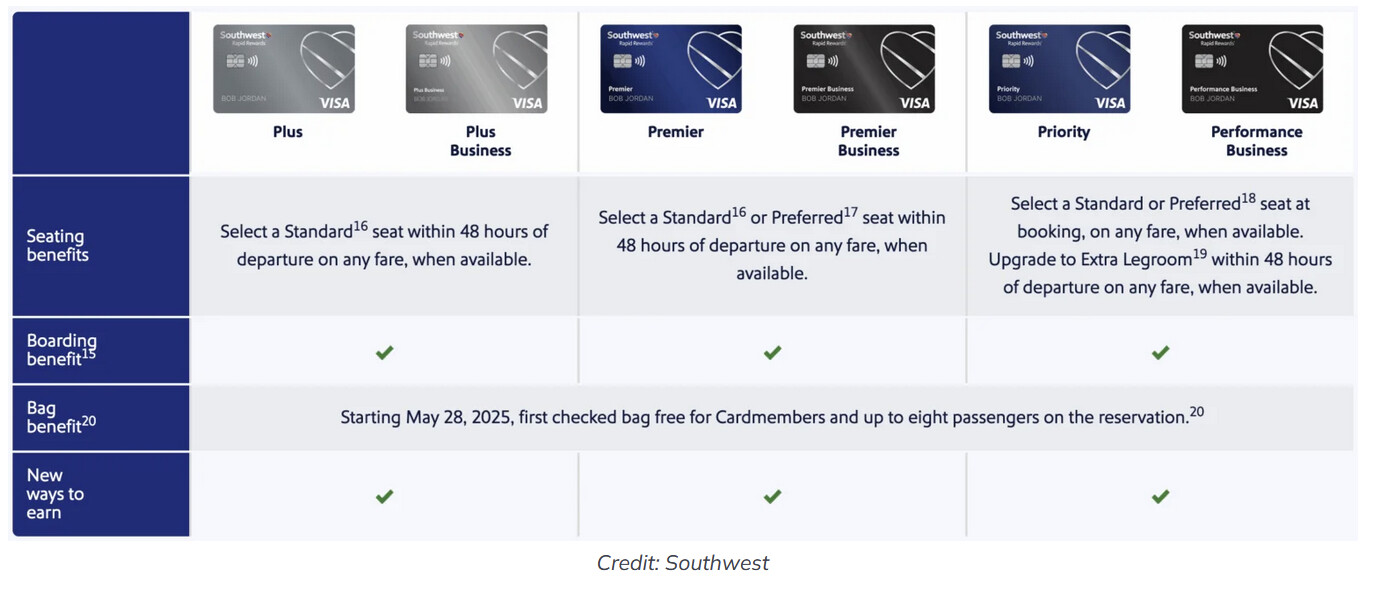

We can start using those card benefits soon! What are the seating assignment benefits? Was that ever ironed out?

1 Like

I believe the personal Priority and the Performance biz are likely the best choice for seat benefits - the more things I can do at booking the better!

I’d wager the extra legroom availability in the 48 hour window will be a tough find on many flights though.

2 Likes

Cross posting from the Liner referral thread -

1 Like

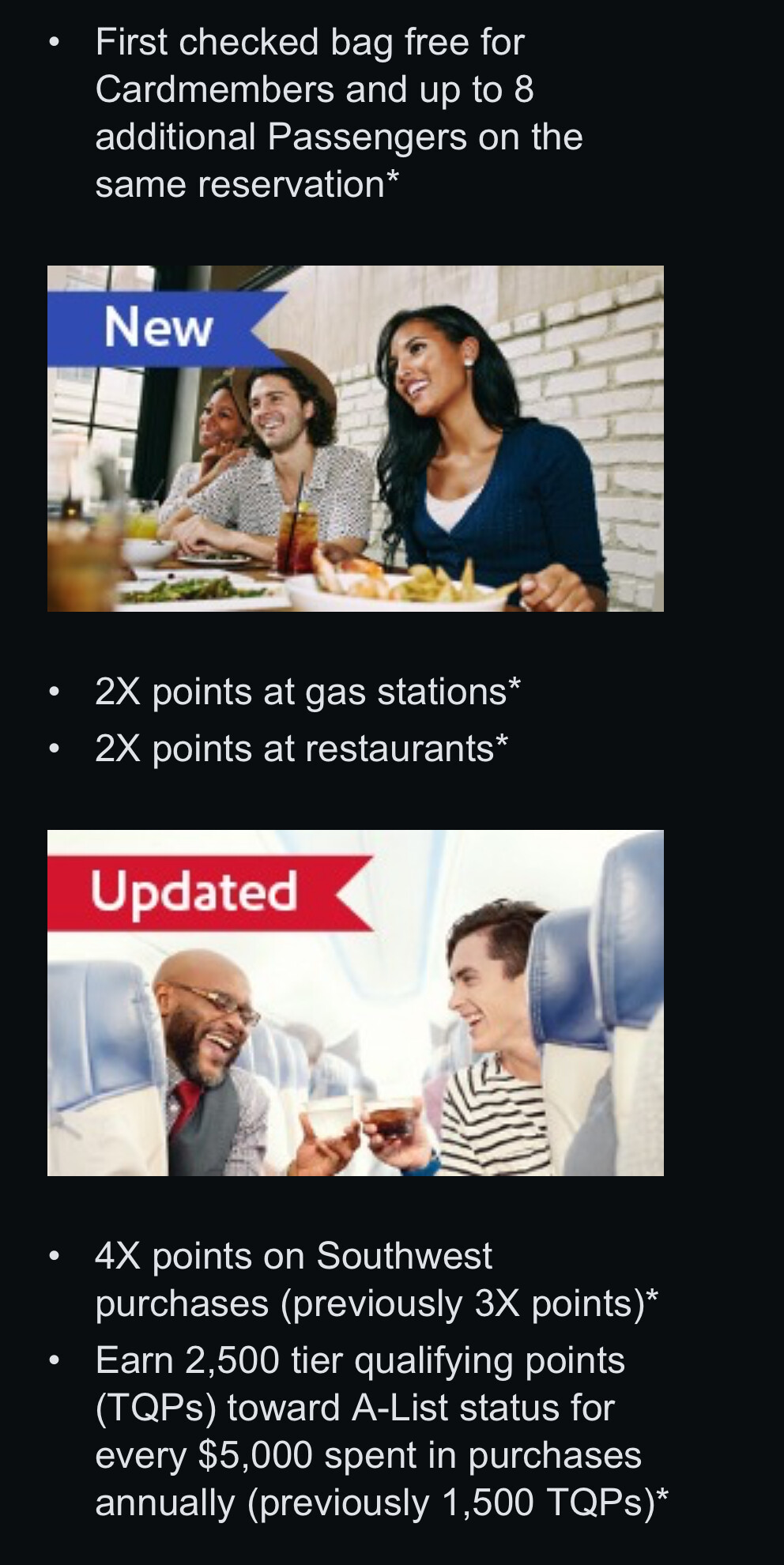

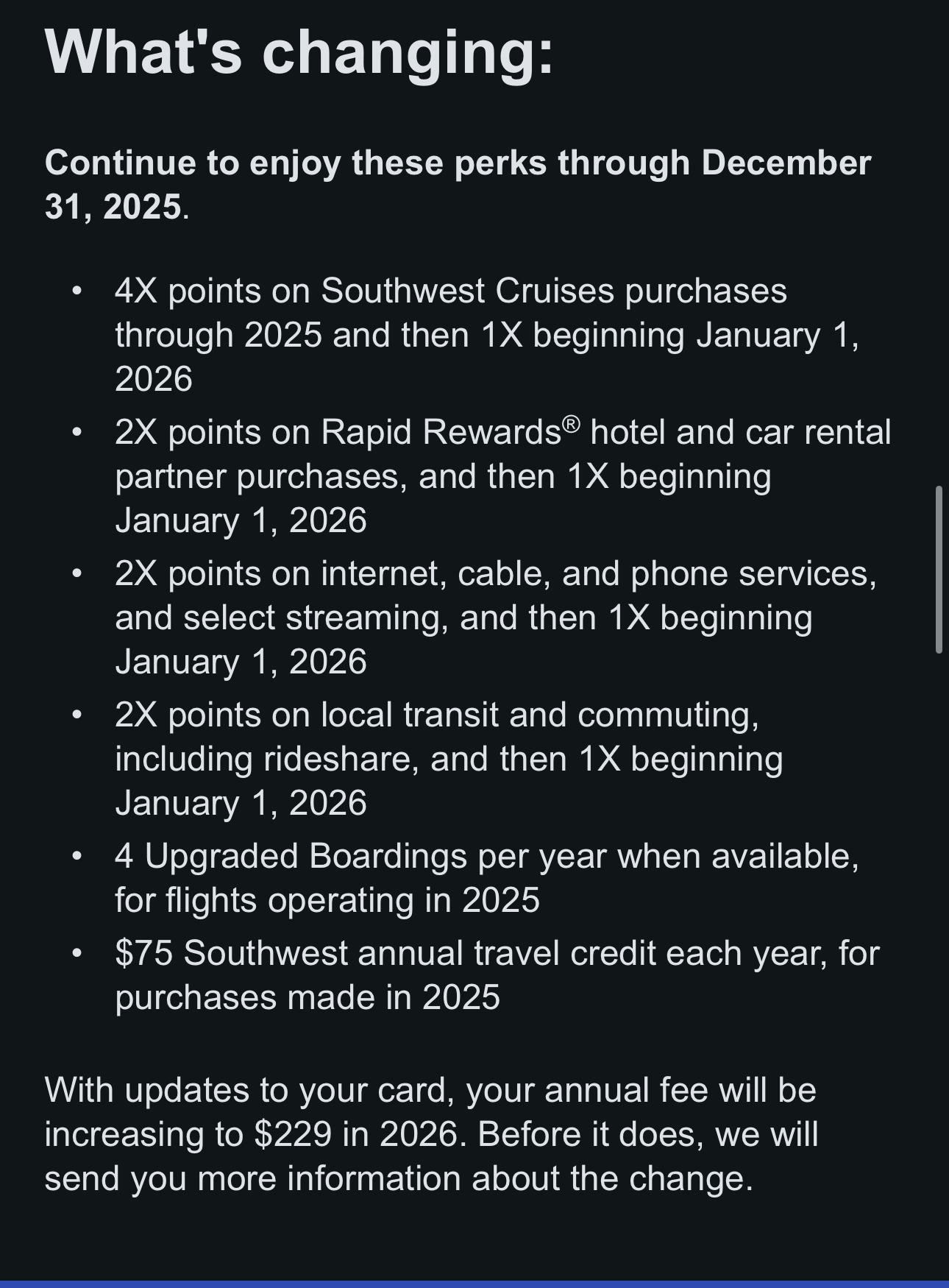

Those increased fees have definitely pushed the value to the edge - I would have thought the anniversary points would inflate at least a little so it didn’t just look like another pure money grab, but they just don’t care about how anything looks these days.

Also, looks like the Performance biz loses free Wifi credits at the end of the year - I know SW was testing free wifi earlier in the year, so guess maybe that can happen. (But, I’d be surprised.)

2 Likes

Right? The anniversary points always kind of made up for the fee. At this point, you’ll need to travel regularly, or with up to 8 people, for the cost of the card to make sense.

1 Like

I guess avoiding the bag fees even once with a family of 4 covers most of the fees on even the higher cost cards.

Could assign some value on the Priority and Perf Biz ability to select preferred seats at booking, too?

But overall: ugh.

2 Likes

I think that’s the only argument for it. It really chafes my *** though as the $99 (now $150?) United cards offered the same free bags and seat selection has always been free for non-basic fares.

I’ll probably hang on to it just for the seat selection aspect, at least until we get a dataset on selecting seats at 48 hours.

2 Likes

I just realized I missed an important change in this offer from the usual ones - this has a 5 month window to hit the spend!

That means if the offer doesn’t get yoinked, you could start this process as early as September for a CP run - rather than the usual late-October.

Hmm, this might make me reverse my application order - I usually go for Biz first just to make sure that gets approved. Mostly unlikely, but Chase can be weird - but in the past I figured if not approved for the Biz I could decide whether I even want a personal.

With recent changes, I do need to have any SW card for the free bags so that tactic is kind of moot. Also, even if I didn’t earn a CP, good to have over 100K more points to shore up my account.

2 Likes

How long do you have to wait after canceling a card to reapply and be eligible for the SUB?

1 Like

Assuming you’ve met other requirements (no SW personal card SUB in last 24 months), usually people say it is safe to wait a week.

But that’s probably overkill.

When I was young(er than I am now ![]() ) and just flipping Disney Visas, I’ve cancelled and reapplied within an overnight day - but I wouldn’t do that anymore.

) and just flipping Disney Visas, I’ve cancelled and reapplied within an overnight day - but I wouldn’t do that anymore.

In reality you can probably go for it in 2 business days - Frequent Miler recently ran a test of this for #science:

2 Likes