The reason you want to keep any new card at least 1 year is related to federal banking rules - paraphrased version: due to rules banks can’t make changes to a card in the first year so they are not fans of customers trying to close or product change. They will very likely claw back any sign up bonus for those that do.

The Freedom cards do not have the points transfer ability to partners that the Sapphire or Ink Preferred cards do.

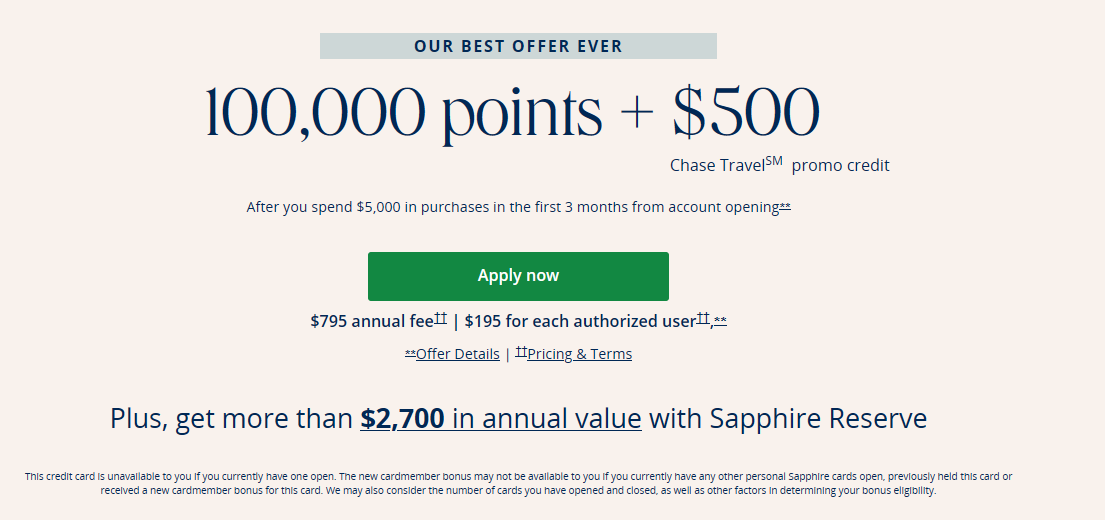

But, when you hold one of those premium cards it unlocks the UR transfers again, so, say you do not need the points for a little awhile AND want to go for another Sapphire SUB, you can downgrade your current card, wait a week or so, apply for the new card.

Also: A nuance in my previous response: I did not suggest product changing to the Freedom Flex but the now-discontinued Freedom with Ultimate Rewards.

It is closed to new applications, but you can product change to it. Sometimes a Chase rep will say you can’t, but just hang up call again. (HUCA.)

Two reasons:

- If you product change to that otherwise unavailable card you leave open the possibility of later earning a SUB on the other Freedom cards. (Although those cards’ SUBs are relatively puny and you may never decide to use a 5/24 slot on them. I have not.)

- The older card is a Visa while the Flex is a Mastercard - so you can use the old Freedom at Costco if that matters to you.

No cost at all to transfer within the household - if you have not done so already, you’ll just need to call or secure message Chase to have them connect both of your cards together. Once you do that, you can move points between your cards online whenever you want.

(I tend to move most points over to me since I hold most of the elevated hotel etc status, so almost always book things from my accounts.)

After all of that, I didn’t address the negative balance: I don’t think that matters at all in the scheme of things. But, if you did close the card they’ll likely cut you a check for the $900 sooner or later. Or, if you did the product change to the Freedom by don’t spend on that card to undo the credit balance, I’m betting Chase will also cut a check after a cycle or two.

Finally: I didn’t mention transferring to United - of course if you know you’ll use the miles there, that’s a good option to think about. The general advice there is not to speculatively transfer miles anywhere from a program like Chase or Amex etc because it is almost always better to keep your options open with the transferrable currency.

But, I’ve broken that rule myself - just last night in fact! (I moved a bunch of Chase UR over to Marriott since they have a 65% transfer bonus until midnight tonight. I’m keeping them out there for future Swolphin stays, hopefully 5-nights at a time to get the 1 free day when I book with points.)