Has anyone else been told by Chase recently that being added as an authorized user counts as one of your 5/24? I was declined for my new Southwest card because my husband recently added me to his United card (to get the bonus signup miles). I’m really befuddled because I would swear I’d always heard AU accounts don’t count for 5/24.

My understanding is AU cards follow same rules as if the card is under your name (counts against 5/24 for personal cards, not for certain business cards).

Yes - there’s a weird nuance to that, but you can get by it.

Happened with my a few years ago and they talk about it on various podcasts once in awhile.

When added as an AU, that card appears on your own credit report and the system (and often the humans) can’t tell that it is an AU account.

When you call recon, you can tell the bank human that it is indeed an AU account and that “I am not responsible for any charges on this card.”

The bank person should be able to take that into account and recon accordingly. Of course, depends on the human, so could take a HUCA or two (Hang Up and Call Again.)

Worked for me when I explained - but then to avoid it for future applications I closed the AU card then asked Experian etc to remove the account. (When I contacted them, they told me to use the dispute function to remove it, took a few weeks to go through. I didn’t try that at first because I did not think “dispute” was what I was doing since it was a valid account before removed.

Alternately, there is info out there on the Googles that you can ask the credit card company to remove it from your report since it is both closed and you were not responsible for the payments. Not sure which might be quicker

These days I do not do AU personal cards at all unless the card is older than 24 months just to avoid all that work. ![]()

If we are trying to hit the spend to earn the bonus on the card and I want both DW and I to work on that together, I’ll give her her the physical card and then add it to my phone wallets so I can just tap and pay.

1 Like

It was the recent United card offer where there were additional bonus points if you added an AU in the first few months so my DH added me. I was turned down on the first call but I’ll try calling again. Kind of a bummer because I closed my SW card to reapply. I don’t suppose they could reactivate the account (it still shows on my account list). Alternatively it occurred to me I could apply for the SW business card. I’ve never tried to get a business card but I’m a doctor and I suppose I might need it to travel to CME seminars.

1 Like

I should have mentioned, I like to have a PDF of my Experian credit report in front of me when I’m talking to the rep - they seem to use that same report, or at least format when looking at your info. That helped me identify things and explain them a little easier when he had questions about when the card was opened etc.

I’d try at least one or two more recon calls before I asked if they could reopen the card - that 100K and potential CP is worth it!

Re: Business card: I think if a professional such as yourself can’t get a business card for their work, many people are in trouble. ![]()

I only do minor outside consulting these days, along with writing for TP, and I’ve had no trouble getting approved.

I’d suggest you use the info in the free 10xTravel course online to see the steps and info you want to provide to apply for a business card. They do a nice job of breaking it down simply.

Long story short on that info: in a business app you not only report potential business income, but also your entire household income as you would for a personal card, so should be a no-brainer for them to approve. (Unless you have set up a company with an EIN, you would apply as a sole proprietor and use your own SSN.)

BUT, one thing: If you get the SW personal card and that puts you over 5/24, that could prevent you from getting the biz card until you drop back under.

Business cards do not add to your 5/24 count, but you normally do have to be under 5/24 to be approved. (Although anything can happen, and co-branded cards do sometimes have laxer approval rules, but that’s not published anywhere.)

1 Like

Thank you so much for your thoughtful advice, I really do appreciate it! I called again and got through to the third layer of Chase, underwriting, and got an agent that I felt really did want to try to help me. But he couldn’t, he said it was a “hard decline” and he could not override. I double checked my report and darn it, there was a card I had forgotten and I was in fact at 5/24 even without the AU until next month. Good news is if I can follow your advice and ditch the AU card I’ll be back under soon. Too late for this SW offer but I’m sure there will be another. The agent assured me I should be able to reinstate my recently closed SW card so then I won’t be without one. I may look into the 10xTravel course. I’ve never delved into business cards because I’m fully employed, but I do have professional expenses that are not reimbursed. I’ve always thought somehow I’d probably be eligible but was too nervous to try. Maybe when I’m back under 5/24 I’ll give it a go! Couple of valuable lessons learned here if nothing else.

2 Likes

Argh, Too bad that forgotten card turned up!

2 Likes

Then I say you qualify. It’s a very easy process. You do not need a business name. So many things qualify for business income and I say expenses related to business count!

1 Like

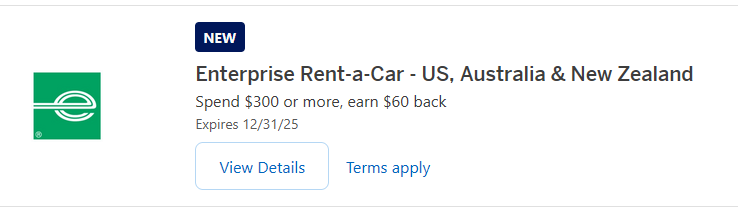

Anyone who watches Amex card linked offers - a couple of nice ones for traveling folk:

- Enterprise Rent-a-car spend $300 get $60 back

- National spend $250 get $50 back.

Don’t forget you have to login and add these to your card for them to be active!

2 Likes

So DW called chase this morning to get the credit for early bird. They gave her some BS that the cycle for the credits starts September 17th, even though that account was opened in August. Probably warrants a HUACA.

2 Likes

You can open the account and get the credit the very next day. So that doesn’t sound right. It should be the anniversary date. Definitely HUCA.

1 Like

How would that make sense even if that statement timing BS were a thing, since you DID already receive ONE of the two credits for the EB you should be getting? Definitely HUCA.

2 Likes

Lots of speculation on the changes coming to the Amex Platinum card along with a $200 annual fee hike.

But even if only a couple of the new credits in the latest Doctor of Credit post show up, this will be a pretty big win!

1 Like

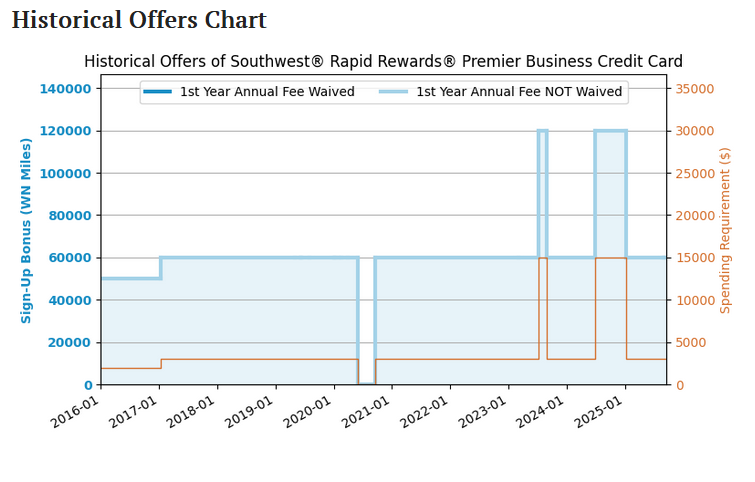

| I am going to bet this is an elevated offer for the business cards, showing up just in time for Companion Pass Season. |

But, if last year’s bonuses for these cards is any indication, I don’t think I’m going to mark this one in the Pro column - while both Biz cards had 120K bonuses last year as well, they also raised the spend from a fairly pedestrian $4K or $5K to a whopping $15k!

IMHO, An extra 40K SW Rewards is so very NOT worth that much extra spend.

Let us proceed with the very tenuous hope that after having increased the card annual fees this year that they temper those crazy spend increases in the hopes that more people go for it.

I doubt they will, but I am manifesting it by speaking it out loud.

(Source on this images is US Credit Card guide, helpful historical charts there for all cards.)

![]() EDIT TO ADD:

EDIT TO ADD: ![]()

Digging a little more on the previous 120K offers, it looks like that US Credit card guide didn’t update their charts to include another instance of them back in March - and Upgraded Points had the following information that makes the elevated spend more palatable.

If the latest bonus is the same, then being able to just spend the $3K for 60K bonus would be a great option to earn the Companion Pass without too much effort.

Also, to reiterate: There is probably no universe where I would then spend an additional $12,000 on that card for 60K more points. Right now, in fact, one could apply for a Chase Ink card and earn 90K Chase UR for “only” $6K spend - and if one wanted could transfer those points to SW later. (Although I wouldn’t do that either.)

2 Likes

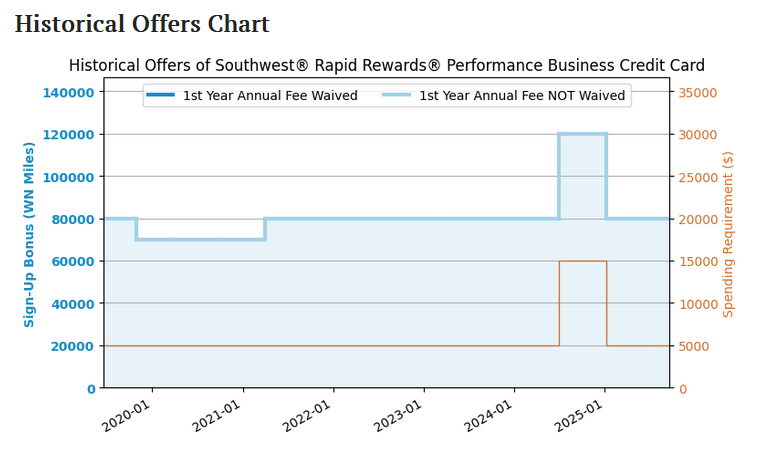

Well, opened up the offer when I arrived home:

120,000 points for the Performance card after $10K spend in 3 months.

So, that’s pretty much a nope.

If one wanted to apply for it, you have to go to: rapidrewardsbizcard.com and enter the invitation code and zip, so I suppose this one might be only targeted? Hmmm.

3 Likes

Back to my credit debacle, I went back and checked the terms and it seems pretty unclear I should have got that credit. The verbiage about “account open date through the first statement” seems like they’re pushing the benefit back a month, likely in anticipation of people using the credits and canceling the card.

“Each anniversary year, you will be reimbursed for the purchase of up to 2 EarlyBird Check-In services made with your Southwest Rapid Rewards® Premier Business Credit Card. Each EarlyBird Check-In service means a purchase made for EarlyBird Check-In one-way, per Passenger. Anniversary year means the year beginning with your account open date through the first statement date after your account open date anniversary, and the 12 monthly billing cycles after that each year.”

2 Likes

Also a no from me.

1 Like

That terms paragraph is ridiculous, but I don’t see how this first sentence:

- …the year beginning with your account open date

could be interpreted as anything but the credit starts immediately?

BTW: Microsoft’s Computer Overlords agree with me.

2 Likes

2 Likes

Oof.

It would have to be a very strategic start date. Like if I had a PIF date for a cruise that by itself would be $4-5000, then I could probably pull off $5000 more with gas and groceries. But we’d 100% need both of us as A/U

3 Likes