Frequent Miler recently did quick rundown on Delta cards and status again, but there’s so much going on for Delta cards even I tune out in the middle of all that info.

But as someone who probably needs to be a Delta flyer might be good to check that out.

From your past info, I don’t feel like you’re into playing the new Sign Up Bonus game that often, and that’s where the real points earning is at.

In lieu of that, might be good to look at your future plans and focus on a small number of new cards that will provide nice benefits and/or nearly free stays or flights that apply to your plans and just go for whatever you feel works into your spending easily.

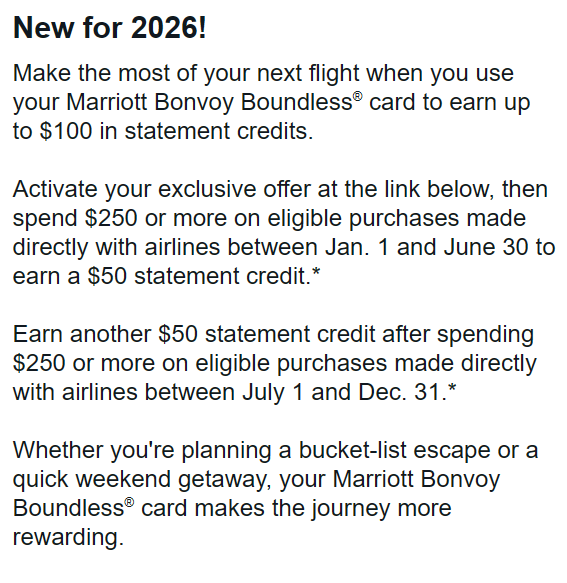

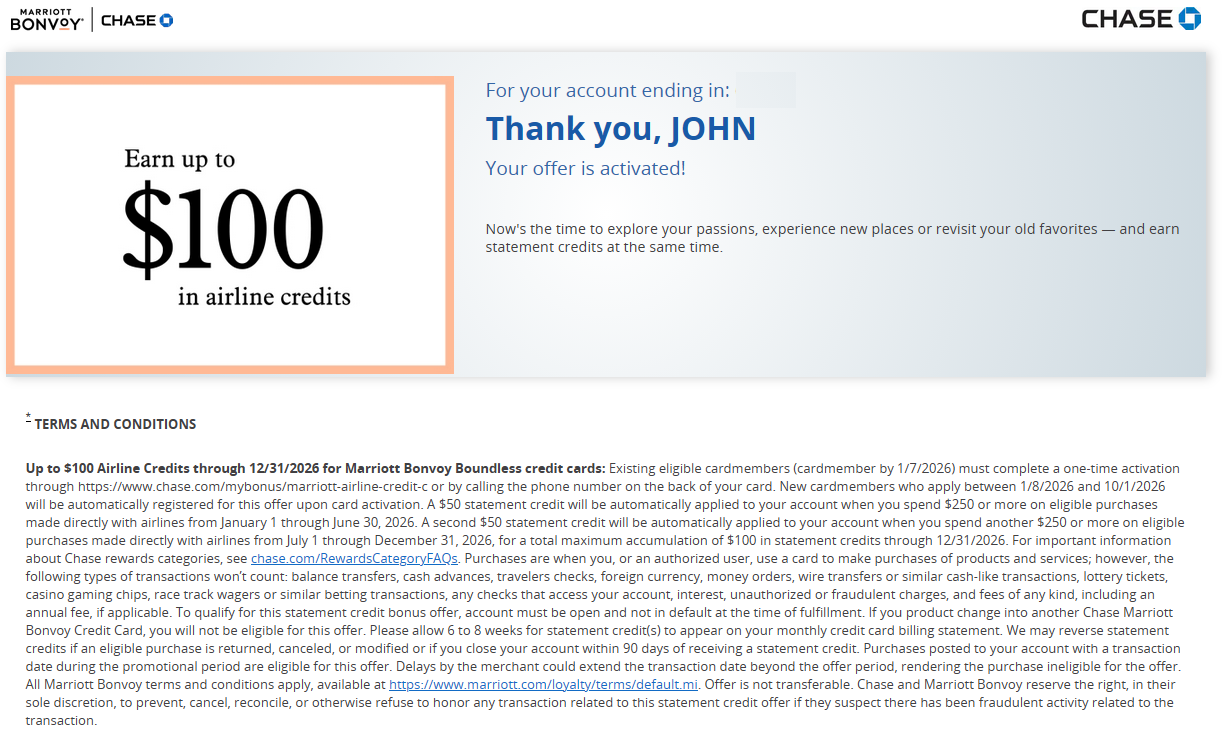

For Disney trips if you can stay at Swolphin and go during lower points times, that Boundless card offer is nice if you can play it right. (Although Marriott still makes you pay resort fees on points/FNC stays.)

Or, in the same line of thought: you could watch for a good bonus on a regular Amex Gold, Biz Gold, etc or Chase Ultimate Rewards card and after earning the Amex or Chase points watch for any good transfer bonuses to Marriott. I used a couple of 70% Chase transfer bonuses to really boost up my Marriott points totals.

To get a feel for how often transfer bonuses happen, you can use Frequent Miler’s search table in this post to see past ones.

Barring all that: If you just want to keep it super simple and just earn the Disney rewards: If you’ve had your Disney Visa more than 24 months, you can cancel, wait a week then reapply and get a bonus.

Usually the best play is 2 player mode:

If you hold the card, refer to your wife for a new one. You get a referral credit, she gets the bonus. If you’re up for holding 2 cards, you could then close your card and use your wife’s referral to open a new one and double it all up. I did exactly that for years before I started playing the larger points game, which has better return.

When getting a new Disney Visa, the math works out that it is best to get the Premier card in year 1 because the higher bonus and higher points earning together outweighs the annual fee. Then, when your annual fee hits again in year 2 you can call or message Chase to downgrade to the no annual fee card.