This could really go in either Universal or Disney, but I didn’t see a good place to post it.

I’ve got about a month before my next Universal trip. A part of my “Disney Refugee’s Year at Universal” budget I included multiple sign-up offers from various credit cards that I’ll pay in full, get the bonuses and then close the account. (This is critical. Plus, you can typically sign-up again for these offers in 12 - 24 months depending on the bank)

IMHO - These weren’t as easy to find as pre-COVID, but I had bookmarked a couple and found one in the mail. I thought I’d share if anyone is looking to do this.

All of these are spend $500 in the first 3 months after sign-up and get $150 - $200 after you pay that initial $500. No Annual Fees…

CAPITOL ONE OFFER - $200 Bonus / Spend $500 in 3 months

https://www.capitalone.com/credit-cards/cash-back/quicksilver/

(This one I got an “invite” in the mail w/ an offer. I’d bet if you call and ask for it they’ll sign you up)

.

.

.

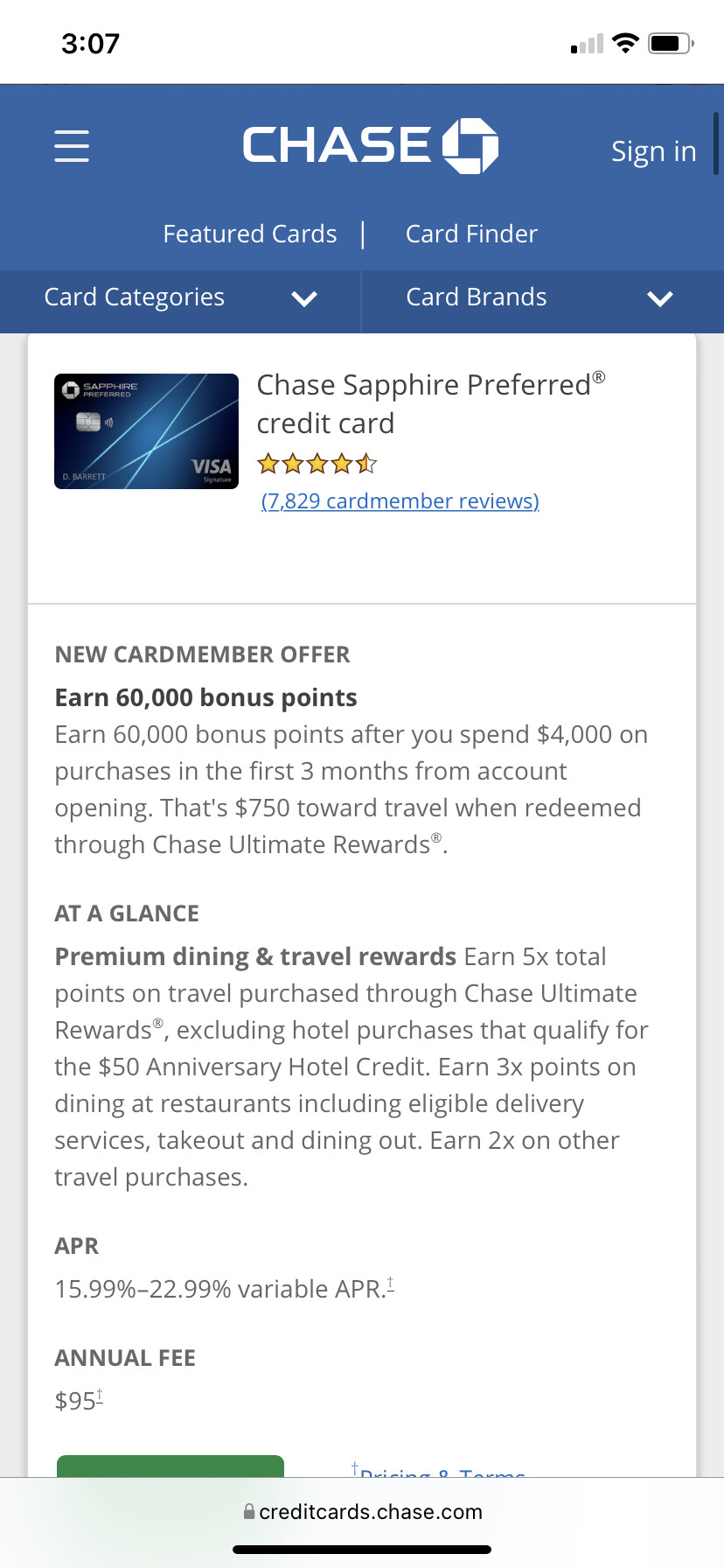

Of course there’s always the Chase Disney Visa Card - It’s only $150 bonus, but no fee and only a $500 spending requirement.

Also, you can get offers for $100 in bonuses for each referral. I just sign-up my wife on her own card, instead of us using the same number. She that gives us her $150 sign-up and another $100 to own main account.

Finally…

The SouthWest Visa gives $200 in sign-upbonuses, but does have a $69 Annual Fee you pay at sign-up. However, there’s no minimum purchase required!!! (That’s still $130 in “free” money)

If you still want to keep the account open and will spend $500 in the first 3 months you’ll get an additional 10K miles as well. (So, it’s really two bonuses for one card! That can make the fee not as hard to swallow.)

Hope this is helpful! I did two today and will do two more once SouthWest opens their fall calendar in a couple weeks. FYI - this isn’t my first time doing this. I promise it works if you just open it, pay in full online and close it.

I’ll be buying Universal gift cards to fulfill my purchase minimums to exactly $500 on each. Then I’ll use the bonuses to do the same. In that way I won’t pay a penny more than required before closing the accounts and all the funds were going to be used at Universal anyway…

I agree. I shouldn’t have to play games to bump my score when, in reality, I’m not changing any actual credit usage.

I agree. I shouldn’t have to play games to bump my score when, in reality, I’m not changing any actual credit usage.