American shines in their intercontinental flights- at least for the first/ business class. My airplane snob boss (his words, not mine) prefers American when he goes to Germany and Italy. But he won’t fly them domestic.

Good to hear they are good at something!

1 Like

I suggest doing this card. Good sign up bonus and as you mention, no annual fee for the first year.

A couple other benefits of this card:

-

They tend to put out no lifetime language offers out for this card often. I recently got my 3rd one in 18 months.

-

It comes with a $150 delta stays credit. This can be used to book and hotel through their portal and can be for 1 night. We’ve even booked, canceled and the credit wasn’t clawed back.

-

It also gives instacart+ free for 6 months. Not a huge perk, but we use it.

4 Likes

Thanks all! Delta has most of the nonstop flights out of MSP. It’s that or Sun Country usually.

I don’t realize the other perks so thanks for that info! The spend seems a bit higher with $6k needed. Might take me longer to get to than I’d like. Maybe some of those summer registrations for my son will help out there, ha! I wonder why others were seeing a lower min spend. I’ll have to look around.

4 Likes

Check by logging into your Amex portal on a computer vs on your phone. While on the computer, check in several different browsers, using the incognito mode or clearing cache after each visit. The Amex offers are all over the place.

Also, look at @JJT list of referral links and see if you get a better offer through those (unless you are being referred by a spouse or family member of course!)

2 Likes

Thanks. I’ll try on the computer. I’ve tried a few ways, but only get different offers for the personal gold card, not the business one. I previously had a gold card that I downgraded to a blue card, so I don’t think I can get that introductory offer again.

2 Likes

This seems bad.

2 Likes

Thanks for this detailed information. I applied and was already approved for Disney Inspire and used the referral link ![]()

I did notice this card doesn’t offer trip cancellation and interruption like the chase flex or unlimited. My thinking is to continue to book my trips on flex or unlimited but pay off at resort with this card just enough to get the credit for the 2k annual requirement. Then I’d likely use target gift cards for the remaining since that beats 3pct. Does this make sense? Anything I am missing short of yet another credit card?

4 Likes

I think that sounds like a good plan!

Of course, any new card sign up bonus will beat spend on current cards, but sometimes it is just best to maximize using what you have. (I’m in that mode right now.)

2 Likes

Heads up to anyone who uses their Amex Platinum airline credits to purchase United Travel Bank (UTB):

There’s a broo-ha-ha going on in various points thread that any UTB credit purchases after Feb 6th have not credited and there is a lot of chicken littling going on that the credit is dead.

While that could be true, in general, there are often slowdowns with Amex credits that occur, so I’d be cautious in believing it is truly a dead tactic yet.

Frequent Miler has a good perspective, as usual:

I happened to be waiting until the end of the year for my Plat credit to make it last as long as possible. If it indeed does turn out to be dead, I guess I’ll be back to using it for SW credits (which already have and don’t need right now), or maybe JetBlue.

Although, JetBlue credits expire within a year, so I’ll need a plan if I go that direction.

3 Likes

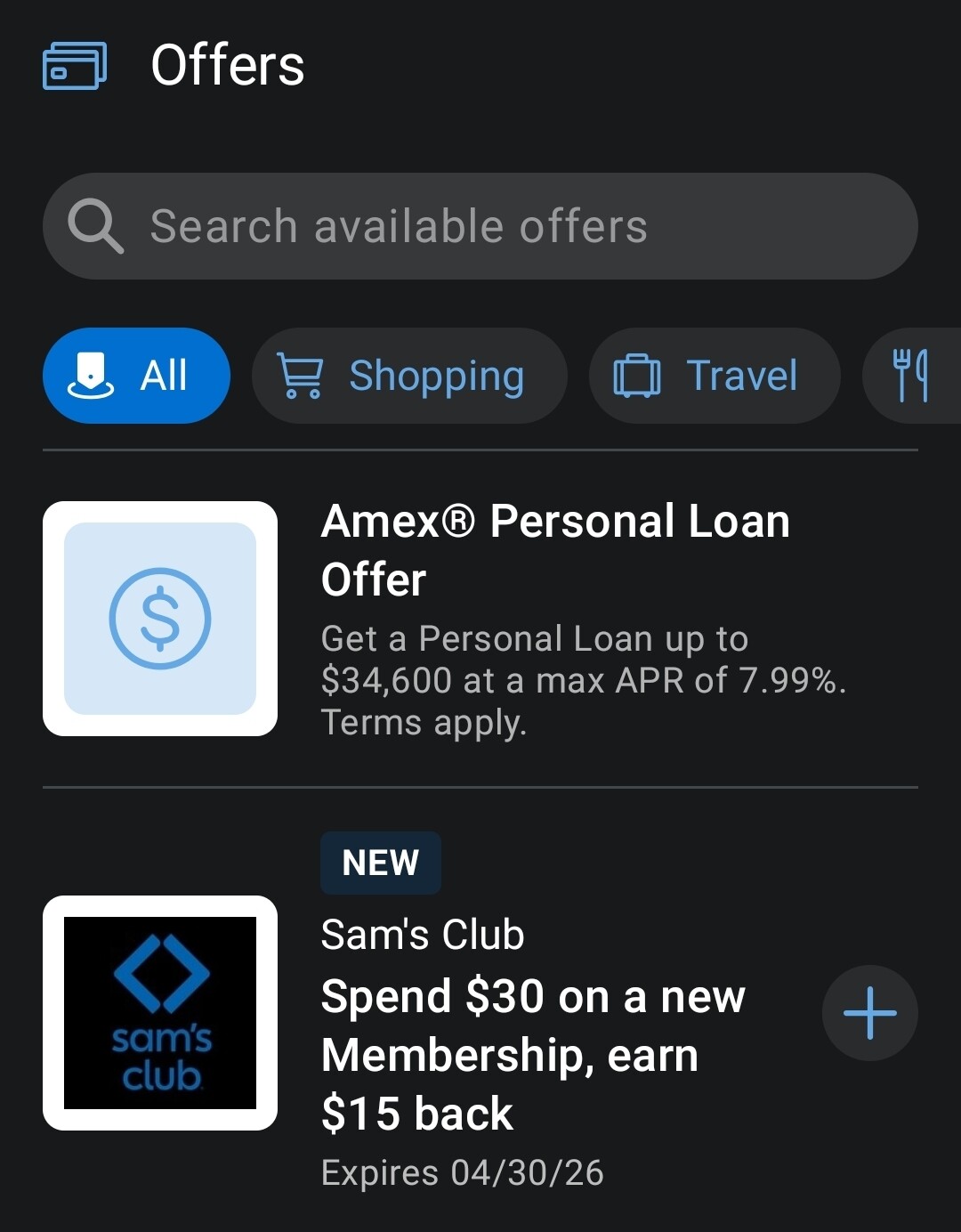

Anyone who digs Sams Club, there’s a possible stack out there for a new membership:

Sam’s has a deal going right now for $50 membership that comes with a $30 Sams credit to spend.

Amex has a Sam’s offer on some of their cards: spend $30 on new membership, get a $15 credit.

(As usual, you need to find that offer on your card and add it there before trying to use it!)

So: Net $5 Sam’s club membership.

Added later: added info from Liner on chat: “With Sam’s, you can add another person who does not live with you as your second member. I have my sister who lives in Florida as mine”

So, net net $2.50? ![]()

3 Likes

I have been meaning to create a post outlining my Hilton Free Night Certificate (FNC) & credit card plan for awhile - here’s a quick rundown of what I’m working on.

First, I’d like to point out that there are currently some elevated bonuses for the Hilton Amex cards for anyone who would like to jump into the Hilton pool with me - perhaps a free multi-thousand dollar Conrad Orlando stay, anyone?

Here’s the current offers:

- Hilton Honors Card: 70K HH + Free Night Certificate after spending $2k in 6 months

- Hilton Surpass: 130K HH + Free Night Certificate after spending $3k in 6 months

- Hilton Aspire: 175K after spending $6k in 6 months

Note that there is NOT a FNC included with the sign up bonus on the Aspire - But you do get an FNC each year as a regular benefit of the card. (It shows up 6-8 weeks after annual fee hits.)

In the last day or so the elevated bonuses hit people’s referral links, so be sure to use your friend or family referral link - or grab one from the Liner referral sheet.

Remember: Amex let’s you pick ANY card from their portfolio, so if you use someone’s link and it doesn’t go directly to the card you want, select Personal cards on the page, then scroll to the Hilton cards down the list. (They will be spaced out.)

Precursor to THE PLAN

Now, obviously Hilton points are not transferable points like Amex MR or Chase UR etc, so technically are not as valuable. You can often do more better by earning points on those other currencies and using them directly or transferring to Hilton etc - when there are bonuses, hopefully.

All of that has been said before back in the thread, so I will not rehash it.

| This year in my house we’re stepping back on new card bonuses because of time management and just to keep things steady since I still don’t have plans to use most of my current stash of various points. |

So, I’m looking to maximize the cool factor on what we might be able to do through credit card spend using cards I already have.

Last year our visit to the Conrad Orlando was a huge, huge hit in my house.

So, I’m working through some not so evil plans to see how many Free Night Certificates I can amass to take another relaxing trip down there.

Before I post my spreadsheet plans, I’m going to point out a few things about the cards:

Surpass card:

- Earns 12x points at Hilton, 6x at Grocery, Gas, Dining, 4x Online and 3x everywhere else.

- Earn a FNC for $15K spend on the card

Aspire Card

- Earns 14x at Hilton, 7x on SELECT Travel, 7x Dining, 3x all else.

- Get one FNC each card year

- Earn an FNC with $30K spend on the card

The Surpass card is a better overall points earner, so when it comes to Hilton cards I mostly use that - especially because I am going to hit them FNC spending tiers.

THE PLAN

I currently hold both a Hilton Surpass and an Aspire card.

In a nutshell, the plan is to spend on the Surpass card to earn the 1 FNC, then continue to spend until just before I hit the 2nd $15K threshold. (Going to replace our front entry and garage doors this year for sure, probably start up a kitchen remodel as well. Yay.)

I will then upgrade the Surpass to another Aspire card and finish off that spend. Since it is technically the same account even though I product changed the card, I will have hit $30K spend on the Aspire and earn a 2nd FNC.

The upgrade to a new Aspire itself should (slight chance it may not) immediately trigger an FNC, because, NEW ASPIRE.

Assuming I can reach those goals before this card’s August annual fee hits - when it does I will get ANOTHER FNC.

Soon after I upgrade that Surpass card to an Aspire I will downgrade my current Aspire to a Surpass. Each of these product changes should result in adjustments to the annual fee for each - Amex will prorate the year and refund or charge accordingly.

So, doing this upgrade/downgrade combo will even out so I net pay the $150 annual fee for a Surpass card and $550 for an Aspire.

It is important to note that each of these cards have various credits -

- Surpass gets a $50/quarter Hilton credit.

- Aspire gets you Diamond status, a $209 CLEARME credit, $200/half resort credit, and a $50/quarter Airline credit.

The Summary Spreadsheet

My worksheet is below - you can see that while I’m paying $700 in annual fees for these cards, if I value the credits on the cards 100% I actually net $204 from the whole shebang.

Now, I really do not value them at 100%, but even so - at worst it is likely a wash when it comes to fees. And that doesn’t include the value of the points earned, receiving Diamond benefits like upgrades, breakfast credits etc.

Most Importantly: Going through these steps I should end up with 5 Free Night Certificates and somewhere in the neighborhood of 150,000 Hilton Honors points. (Worth about 1.5 nights at the Conrad, or 3 or 4 nights in a lower level Hilton.)

3 Likes

If anyone reads messages in points and travel groups, so much complaining about various Southwest weirdness with boarding, bags, not allowed to change seats, blah blah.

But, maybe some decent fixes coming:

4 Likes

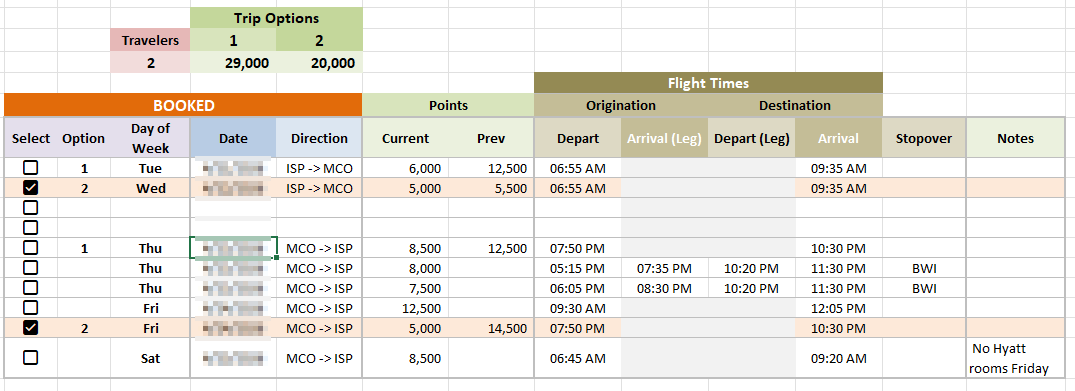

Anyone with Southwest flights, might be time to garden your reservation & check sale price changes. this weeks numbers seem a lot better than previous weeks’ changes:

I have one placeholder trip in April where a Friday night flight home from MCO was stuck at 14,500 points for months and just dropped to 5,000 today. Also the Wed flight down dropped from 5,500 to 5,000.

14,500 was #painfulpoints so I had originally booked other days that were less desirable for my calendar, but saved a bunch of points. Now, this new combo saves me 9,000 points over those flights!

2 Likes

We have spring break flights that are criminally high, and I’ve not seen them go down in month. I check twice daily. The lowest it’s gotten down to is 14k for a flight coming in at 12am to FLL.

Fall break flights are still quite high, but we’re still seven months out. We’re unfortunately locked in our dates but even the day before/after is wild. If something for 5,000 came around I’d faint!

2 Likes

That stinks. These flights I changed are nearer the end of April, so maybe at that point I’ve edged out past the active Spring Break madness window.

Edit to add: I just realized I did not check another placeholder trip I have booked at the start of May (not sure exactly when DS and I can jump down for a round of golf yet.) - and those flights jumped UP in points from 5500 to 7500 on the way down and from 8500 to 12500 on the way up!

Crazy algorithms.

2 Likes

I am stressing. In the before times, I would have booked our SW flights a few months ago for 4/25 - 5/2. Then I would keep rebooking as I watched the price go down and receive non-expiring travel credits. (I did read your earlier posts about the hack for making expiring credits into non-expiring, but I would rather not deal with that if I could avoid it). The flights I am looking at are obviously in demand and have remained high in price. I have read in more than one article that 56 to 44 days out is the sweet spot for booking flights, so I am trying to be patient. But it is getting close (Day 53). I check 3 or 4 times per day using incognito mode and I clear cookies beforehand. While other flights have dropped, the ones I want have not. When they have dropped, there are only 1 or 2 seats available at that price. I am worried now about seat selection. I have the SW Priority card.

1 Like

We all definitely need to put in the time to see if we can find any SW patterns - so far I have no idea, so I’m just logging the prices in my Excel table and just keep checking a few times a week.

I have about $350 in travel credits out there to use too, but I so seldom have a trip locked in far in advance that I haven’t even tried to use them yet. Hardly worth using them when booking in a short window after they balloon the prices up. One of these days.

1 Like

@drvillarejos — I used your referral link today and was approved for the CSR. Thanks!

4 Likes

Thank you! I love the rewards on that card. I’ve had some nice stays on Hyatt points too!

1 Like